Profitability is still an exception in the U.S. cannabis industry, not the rule. Most multi-state operators continue to post losses, carry heavy debt loads, and fund operations through dilutive stock issuances - all while watching wholesale prices soften and tax bills climb. Green Thumb Industries has taken a different path. Through disciplined expansion and tight operational control, the company has built one of the few genuinely profitable businesses in licensed cannabis retail, a distinction that carries real weight as the broader sector works through a prolonged period of margin pressure.

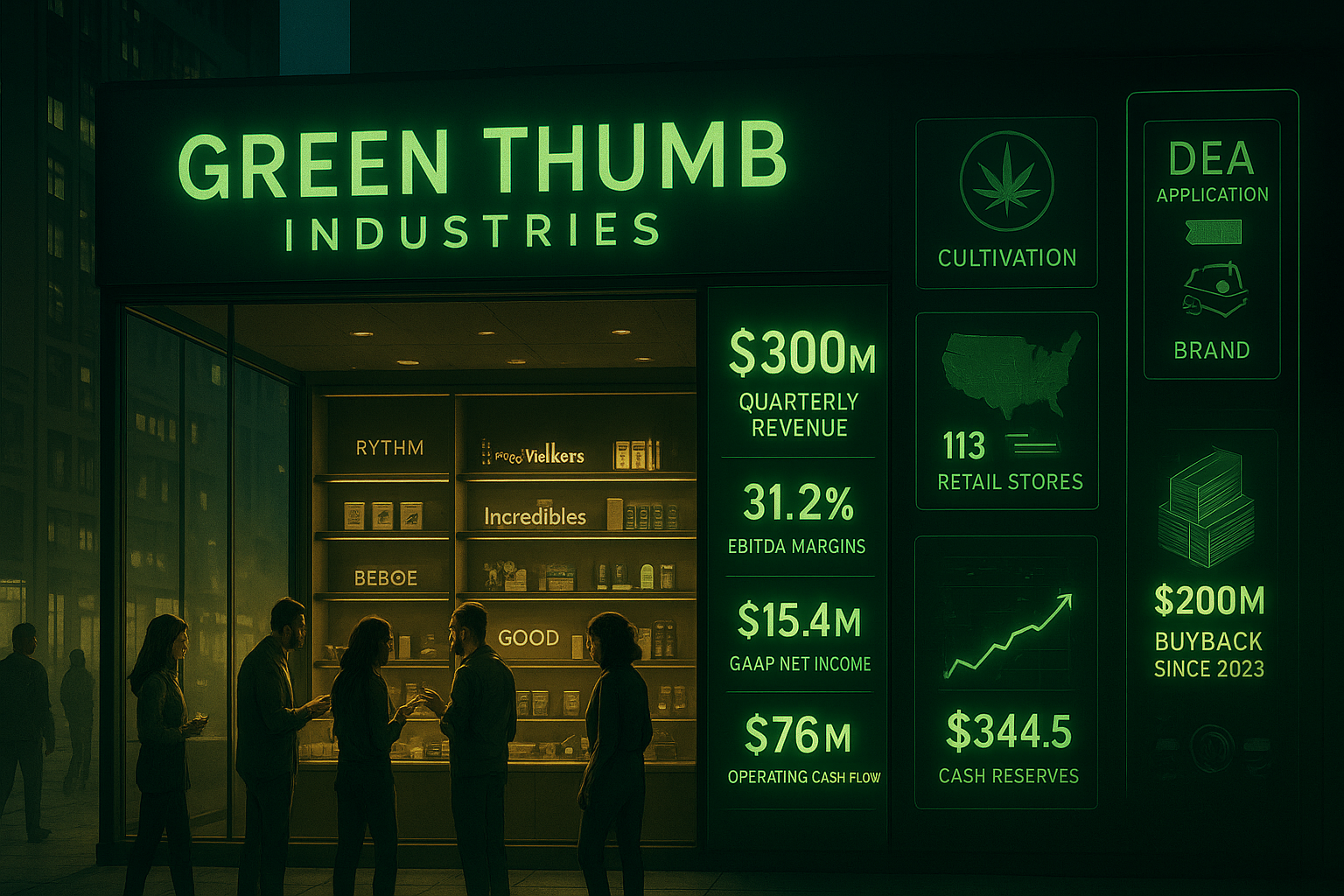

The financials behind that claim are specific. In the first quarter of 2026, Green Thumb reported $300 million in revenue - up 7.4% year over year - alongside $15.4 million in GAAP net income, $76 million in operating cash flow, and $93.5 million in normalized EBITDA at a 31.2% margin. For operators tracking their own unit economics, those EBITDA margins are a useful benchmark; most vertically integrated multi-state operators would be grateful to land in the low twenties. The company closed 2025 operating 113 retail stores across 14 states, having opened 12 new locations during the year. For those following expansion dynamics in specific markets, you can read more about what licensed retail growth looks like in one of the country's most closely watched adult-use environments.

Section 280E Remains the Industry's Most Punishing Structural Problem

Here's the thing every cannabis operator understands at a visceral level: Section 280E of the Internal Revenue Code doesn't just reduce margins - it inverts the basic logic of business taxation. Because cannabis remains a Schedule I controlled substance at the federal level, licensed operators cannot deduct ordinary business expenses the way every other retail business can. That means payroll, marketing, occupancy costs, and administrative overhead all get paid from pre-tax dollars. The effective tax rates that result aren't slightly higher than normal; they can run multiples of what a comparable non-cannabis retailer would owe. For an already margin-compressed business, that structural burden is severe.

The proposed rescheduling of medical cannabis from Schedule I to Schedule III would change that calculus - at least for qualifying medical operations. If the DEA process moves forward as expected, businesses meeting the new framework's criteria would likely exit 280E's reach, unlocking the ability to deduct standard operating expenses. Green Thumb has already filed DEA applications to position its medical business for that framework. The company doesn't need the change to stay profitable; it's already profitable without it. But the removal of 280E exposure on the medical side would directly improve net income and free cash flow, without a single additional store opened or SKU added to a wholesale menu.

A Balance Sheet Built for an Industry Where Banking Is Still Complicated

Access to conventional banking and credit remains one of the most persistent structural disadvantages in licensed cannabis retail. Most federally chartered banks won't touch cannabis operators, which means many companies have limited options when they need capital - expensive private debt, equity dilution, or sale-leaseback arrangements on real estate are common workarounds. Green Thumb has largely sidestepped that bind by generating cash internally. The company ended the first quarter with $344.5 million in cash and an expanded syndicated credit facility, giving it flexibility that smaller operators simply don't have.

What's striking here is how management has chosen to deploy that strength. Since September 2023, Green Thumb has repurchased roughly 29 million shares for approximately $200 million - an aggressive buyback program that would be unremarkable at an S&P 500 company but is genuinely unusual in cannabis. Share repurchases signal something specific: that management believes the stock is undervalued and that internal capital allocation beats putting that cash into marginal new store openings or speculative market entries. For industry observers, it also signals that the company isn't being forced to dilute existing shareholders to keep the lights on, which is more than many competitors can say.

What This Means for the Broader Cannabis Retail Sector

Green Thumb's performance doesn't erase the structural pressures that every licensed cannabis retailer faces. Price compression in maturing adult-use markets is real. Excise tax structures in states like California and Illinois have made it harder for compliant operators to compete against the illicit market on price. Regulatory environments shift - licensing freezes, local opt-outs, and compliance cost increases can affect store-level economics with little warning. None of those risks disappear because one operator is managing them well.

But Green Thumb's financial profile does illustrate something important for operators at every scale: vertical integration, brand development, and balance sheet discipline aren't just theoretical advantages. They show up in EBITDA margins, in the ability to fund new store builds without taking on crippling debt, and in the capacity to weather pricing cycles without emergency fundraising. Its consumer brands - RYTHM, Dogwalkers, incredibles, Beboe, and Good Green - hold positions in several of the country's largest legal markets, which provides wholesale revenue streams that purely retail-focused operators don't have. For dispensary owners watching how the larger operators run their businesses, the operational takeaway is straightforward: the companies generating cash are the ones with the most options when conditions get difficult. That's not a coincidence.