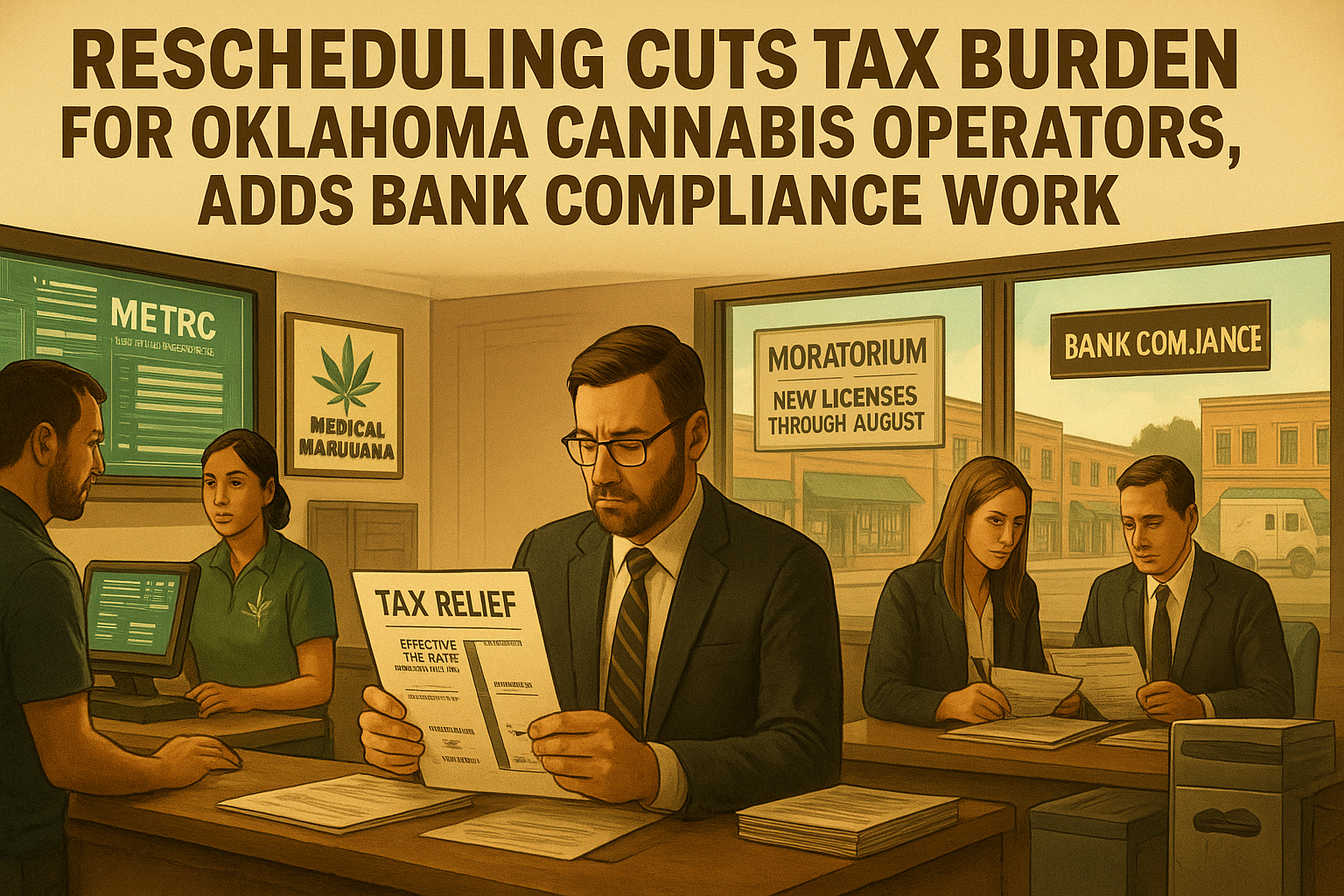

Federal cannabis rescheduling is producing two distinct effects inside Oklahoma's medical marijuana market: real tax relief for licensed operators squeezed by years of punishing federal tax treatment, and a new layer of compliance obligations for the financial institutions that service their accounts. Industry attorneys and compliance specialists are already advising clients on both fronts, with the administrative and financial implications arriving at roughly the same time.

The most immediate financial change is the elimination of Internal Revenue Code Section 280E. Under Schedule I status, cannabis businesses could only deduct the cost of goods sold - payroll, rent, utilities, and other standard operating expenses were nondeductible, effectively taxing gross profit rather than net income. The provision has a specific origin: Congress enacted 280E after the IRS lost a 1980s case in which a Florida cocaine trafficker successfully deducted the cost of cigarette boats and aircraft as business expenses. As Eric Fisher, director at Crowe and Dunlevy law firm and a former banker, has explained, the rule went largely untested until state medical marijuana programs created a class of businesses actually filing tax returns. With cannabis now classified under Schedule III, that restriction lifts. "It's no longer an illegal drug; it's a scheduled drug," Fisher said. For dispensary operators who have been absorbing the 280E penalty for years, the difference in effective tax rate can be substantial - and for tightly margined operations, it may determine viability. Systems built to document compliant retail operations - from cannabis dispensary pos maine implementations to multi-state POS deployments - will need to align accounting workflows with the new deductibility rules, since expense categorization now carries direct tax consequence.

Here's the catch, though: rescheduling does not mean deregulation. Cannabis remains a federally controlled substance under Schedule III, and banks holding cannabis business accounts are still required to file Suspicious Activity Reports under 2014 Financial Crimes Enforcement Network guidance. That FinCEN framework distinguishes between direct marijuana businesses - dispensaries, cultivators, processors - and indirect ones, meaning vendors, landlords, and professional service providers whose revenue flows from cannabis-adjacent relationships. Stacy Litke, vice president of banking programs at compliance firm Green Check, oversees programs built around that guidance. Dispensaries rely on seed-to-sale tracking through Metrc to generate the documentation banks attach to deposit records, creating a compliance chain that runs from the point-of-sale terminal through the financial institution's own reporting infrastructure. Banks that serve cannabis clients cannot simply absorb the 280E news and move on - their SAR obligations are unchanged, and the documentation burden remains.

Oklahoma's Market Adds Structural Pressure on Top of Federal Changes

Federal policy shifts land differently in Oklahoma than in most regulated cannabis states, and the reason is structural. The state's relatively open licensing framework produced a significant surplus of operators. Average monthly sales per operator have fallen to roughly $80,000 - a fraction of the $600,000 to $1 million per-store figures seen in states with tighter license caps. Wholesale pricing has compressed accordingly. Litke has been direct about the dynamic: "Oklahoma from the beginning has had way too many operators, way too many licenses, way too much product." The state has extended a moratorium on new dispensary licenses through at least August, with a permanent cap under consideration. That kind of market correction - licensing discipline imposed after the fact - is a familiar pattern in cannabis regulation, but Oklahoma got further down the road before pulling back than most states did.

What that means operationally is that the 280E relief, while meaningful, arrives in a market where margins are already under pressure from oversupply and compressed wholesale menus. For many Oklahoma operators, the tax savings may ease cash flow without fundamentally changing the competitive math. The businesses most likely to benefit are those that have survived long enough to have real operating expenses worth deducting - payroll-heavy stores with compliance staff, security costs, and meaningful rent obligations. Smaller or newer operators with lean structures may see a more modest impact.

Cash Still Dominates, but Payment Infrastructure May Be Shifting

Cash accounts for roughly 68% of cannabis transactions nationally. Mastercard and Visa both prohibit cannabis-linked transactions on their networks, which means dispensaries continue to operate under cash-handling burdens that most licensed retail categories left behind decades ago. The physical and operational risks are real - Fisher noted that an operator carrying $300,000 in cash "in all likelihood" has either personal concealed carry or armed security on hand. That is not a hypothetical. It is standard operating procedure in a sector that cannot access ordinary commercial banking and payment services at full scale.

Fisher anticipates that upcoming Treasury Department guidance will open credit and debit card adoption more broadly. That would be a meaningful shift - not just for consumer convenience, but for compliance logging, fraud reduction, inventory reconciliation, and the general operational hygiene that comes with traceable transactions. Cash-heavy environments create friction at every point in the compliance chain, from the point-of-sale log to the bank deposit record to the SAR filing. Broader card acceptance, if it materializes, would also reduce the security exposure that armored-cash operations currently require. The industry has been waiting on that guidance for a long time. Whether the current regulatory moment actually delivers it remains to be seen.